Summary

Fraud is a major problem for Medicare, with over 7% of overall Medicare spending classified as improper payments (CMS, 2024). The case of ambulance rides provides an ideal setting to understand the challenges and opportunities for dealing with such fraud: while Medicare pays for ambulance rides only when a patient is too sick to travel safely by any other means, the program’s generous ambulance payments entice unscrupulous providers to bill for unnecessary rides.

The government has two broad strategies for preventing fraud. With litigation, prosecutors seek to recover money and punish fraudsters through criminal and civil suits after the fraud has already taken place, potentially deterring others from engaging in similar behavior. With regulation, improper payments are instead blocked from being made in the first place. Although economists have often argued that targeted litigation can be less costly and more effective than indiscriminately imposed rules, the relative effectiveness of the two approaches in U.S. health care had not been previously tested on a large scale.

In this paper, we examine this question for non-emergency ambulance transportation for dialysis patients. From 2003 to 2014, the use of this service grew rapidly, and various Department of Justice district offices pursued dozens of criminal and civil lawsuits against ambulance companies accused of fraudulent billing. In an attempt to clamp down on unnecessary rides, Medicare introduced a prior authorization requirement in 2014. The staggered rollout of these efforts allowed us to identify the effects of both anti-fraud strategies.

Prior authorization was much more effective at deterring fraud than litigation was on its own. Spending on non-emergency ambulance rides fell by roughly two-thirds almost immediately following the start of prior authorization. By contrast, criminal prosecutions produced only modest reductions in spending, and civil lawsuits had no measurable impact. Importantly, these savings did not come at the expense of patient care.

To explain these results, we consider a simple model of the decision to commit fraud, where the key factors are the probability of getting caught and the penalties levied as punishment. In the ambulance market, neither of these key parameters was sufficiently high, which meant that the temptation to overbill remained strong.

Regulation overcame both limitations of litigation; it was able to effectively deter fraud by raising the probability that illegal behavior was detected and by automatically applying the penalty. Furthermore, the cost of administering the prior authorization regulation is much lower than the cost of running enough anti-fraud lawsuits to contain fraud. We calculate that if the prior authorization program had been implemented nationally in 2003, Medicare would have saved about $4.8 billion at a cost of less than $30 million annually.

Our study supports the idea that prior authorization can be an effective deterrent to health care fraud and also has implications beyond health care. The government faces the same challenge in many areas of public spending: limited capacity to investigate thousands of small, potentially opportunistic actors and difficulty collecting penalties once fraud is detected. In such cases, litigation is likely to be ineffective relative to regulation.

Main article

This research tests, for the first time, the relative effectiveness or litigation and regulation in targeting the significant issues of fraud within the U.S. health care system. The study uses extensive data on the use of non-emergency ambulance transportation patients for dialysis patients and takes advantage of the staggered roll out of efforts to prevent fraud in this area. Results show that regulation (which here took the form of prior authorization for payments) was much more effective at deterring fraud than litigation was on its own—and savings did not come at the expense of patient care. These findings have implications for many other areas of government spending.

Fraud is a major problem for Medicare. For example, in 2024, over 7% of overall Medicare spending was classified as improper payments (CMS, 2024). The case of ambulance rides provides an ideal setting to understand the challenges and opportunities for dealing with such fraud.

In 2024, over 7% of overall Medicare spending was classified as improper payments.

While Medicare pays for ambulance rides only when a patient is too sick to travel safely by any other means, the program’s generous ambulance payments entice unscrupulous providers to bill for unnecessary rides. From 2003 to 2017, Medicare spent $7.7 billion reimbursing more than 37 million non-emergency ambulance rides for patients traveling to and from dialysis facilities, many of whom could have safely taken a car or public transportation instead. Dozens of operators were eventually convicted of defrauding the government by billing for this unnecessary care.

The government has two broad strategies for preventing fraud. With litigation, the so-called “pay-and-chase” model, prosecutors seek to recover money and punish fraudsters through criminal and civil suits after the fraud has already taken place, potentially deterring others from engaging in similar behavior. With regulation, improper payments are instead blocked from being made in the first place. Although economists have often argued that targeted litigation can be less costly and more effective than indiscriminately imposed rules, the relative effectiveness of the two approaches in U.S. health care had not been previously tested on a large scale.

A natural experiment in enforcement

The government has two broad strategies for preventing fraud: litigation and regulation.

In Eliason et al. (2025), we examine this question for non-emergency ambulance transportation for dialysis patients. From 2003 to 2014, the use of this service grew rapidly, and various Department of Justice district offices pursued dozens of criminal and civil lawsuits against ambulance companies accused of fraudulent billing. In an attempt to clamp down on unnecessary rides, Medicare introduced a prior authorization requirement in 2014 whereby providers needed to submit documentation proving that each patient genuinely required an ambulance before receiving payment. The policy was piloted in New Jersey, Pennsylvania, and South Carolina and later extended to nearby states.

The staggered rollout of these efforts allowed us to identify the effects of both anti-fraud strategies. Using comprehensive Medicare claims data for patients with end-stage renal disease combined with hand-collected data on federal lawsuits, we investigated the impacts of both litigation and regulation on health care spending, ambulance companies, and Medicare beneficiaries.

Regulation was much more effective than litigation

Prior authorization was much more effective at deterring fraud than litigation was on its own.

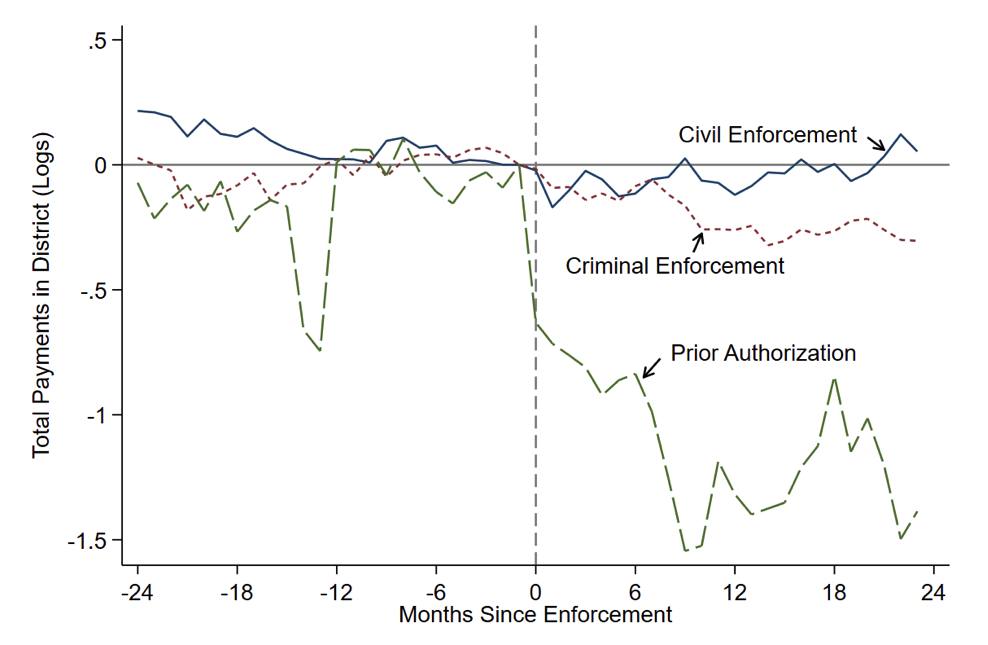

Prior authorization was much more effective at deterring fraud than litigation was on its own. As shown in Figure 1, spending on non-emergency ambulance rides fell by roughly two-thirds almost immediately following the start of prior authorization. By contrast, criminal prosecutions produced only modest reductions in spending, and civil lawsuits had no measurable impact.

Figure 1: Effect of Prior Authorization Regulation and Civil and Criminal Litigation on Non-Emergency Ambulance Spending

Note: Figure reports estimates of the effect of prior authorization, civil litigation, and criminal litigation on Medicare spending (measured in logs) as reported in Eliason et al. (2025).

Spending on non-emergency ambulance rides fell by roughly two-thirds almost immediately following the start of prior authorization.

In addition to causing a large drop in the number of non-emergency ambulance rides to dialysis facilities, prior authorization also led to substantial changes in the market for ambulance services. We find that the number of ambulance companies fell sharply in response to prior authorization and that those that remained in operation became more specialized in providing only non-emergency dialysis rides.

Importantly, these savings did not come at the expense of patient care: dialysis adherence, hospital admissions, and mortality rates were unchanged, even for patients who previously relied heavily on non-emergency ambulance transportation. Following prior authorization, riders were more likely to appear genuinely unwell, suggesting that the policy improved targeting without restricting access for patients in need.

Why “pay-and-chase” fell short

To explain these results, we consider a simple model of the decision to commit fraud, including the probability of getting caught and the penalties levied as punishment.

To explain these results, we consider a simple model of the decision to commit fraud, where the key factors are the probability of getting caught and the penalties levied as punishment. In the ambulance market, neither of these key parameters was sufficiently high. Out of more than a thousand firms suspected of overbilling, only a few dozen ever faced prosecution. That is, fraudsters faced a very low probability of detection. Even in cases where fraudsters were successfully prosecuted, they faced limited liability, often paying back less than half of the judgments made against them, as small companies could dissolve without paying restitution. With such low expected costs of cheating, the temptation to overbill remained strong.

Regulation overcame both limitations of litigation. Because providers could no longer be reimbursed without prior approval, illegitimate claims were much more likely to be detected and not paid out, eliminating worries about the difficulty of collecting funds after the fact. This upfront review could be conducted by specialized monitors, avoided the evidentiary hurdles of criminal prosecution, and did not depend on recovering money from defunct firms. In contrast to pay-and-chase litigation, upfront regulation was able to effectively deter fraud by raising the probability that illegal behavior was detected and by automatically applying the penalty.

Our study supports the idea that prior authorization can be an effective deterrent to health care fraud and also has implications beyond health care.

Furthermore, the cost of administering the prior authorization regulation is much lower than the cost of running enough anti-fraud lawsuits to contain fraud. We calculate that if the prior authorization program had been implemented nationally in 2003, Medicare would have saved about $4.8 billion at a cost of less than $30 million annually. By contrast, each anti-fraud lawsuit costs the government roughly $250,000, and we find that the $6.5 million spent since 1998 on litigating civil cases against ambulance companies did not deter others.

Policy implications

Our study supports the idea that prior authorization can be an effective deterrent to health care fraud and also has implications beyond health care. In many areas of public spending, from pandemic relief loans to disaster-recovery funds, the government faces the same challenge: limited capacity to investigate thousands of small, potentially opportunistic actors and difficulty collecting penalties once fraud is detected. In such cases, litigation is likely to be ineffective relative to regulation. In future work, we study the related effects of competition on deterring fraud.

This article summarizes ‘Ambulance Taxis: The Impact of Regulation and Litigation on Health Care Fraud’ by Paul Eliason, Riley League, Jetson Leder-Luis, Ryan C. McDevitt, and James W. Roberts, published in the Journal of Political Economy in May 2025.

Paul Eliason is at the University of Utah. Riley League is at the University of Illinois Urbana-Champaign. Jetson Leder-Luis is at Boston University. Ryan C. McDevitt and James W. Roberts are at Duke University.

References

Centers for Medicare & Medicaid Services (CMS). Fiscal Year 2024 Improper Payments Fact Sheet. Nov. 15, 2024. Retrieved from https://www.cms.gov/newsroom/fact-sheets/fiscal-year-2024-improper-payments-fact-sheet

Eliason, Paul, Riley League, Jetson Leder-Luis, Ryan C. McDevitt, and James W. Roberts. 2025. “Ambulance Taxis: The Impact of Regulation and Litigation on Health Care Fraud.” The Journal of Political Economy 133, no. 5 (May): 1661-1702. https://doi.org/10.1086/734134