Summary

Global renewable electricity generation has grown dramatically over the past decade, but most recent growth comes from intermittent sources like solar photovoltaics (PV). This intermittency reduces the benefits of renewables because—where energy storage is not available—it intensifies the need for quickly adjustable and dispatchable types of generation, which are typically emission-intensive fossil fuel plants.

Battery storage offers a promising solution: it can store excess energy when renewable output peaks and release it when production drops, ultimately lowering the overall costs of meeting electricity load. However, while battery costs have fallen sharply, capital costs remain a major barrier to utility-scale storage.

To understand the role that battery storage is likely to play in the future, we build a framework to understand both how batteries operate in the electricity market and how potential battery operators decide whether to add capacity to the grid. We apply our framework to data from California—a state at the forefront of renewable energy production—that covers the period 2016-19, which saw dramatic growth in renewable generation.

Our framework also captures how electricity markets would behave if far more battery storage were operating than we observe. This matters because, as batteries become more common, they naturally smooth out extreme price swings—which, somewhat paradoxically, reduces the profits batteries can earn from buying low and selling high.

We find that a small amount of battery storage would be profitable even without subsidies, but large-scale investment remains dependent on continued policy support because of the paradoxical effect noted above. These diminishing returns are quantitatively large. At a 50 percent renewable share, average value per kilowatt-hour falls from about $280 for a 10 MWh fleet to $230 for 10,000 MWh and just $140 for 50,000 MWh.

Our study also models how battery adoption may evolve under different policy and market environments. We find that a major determinant of future adoption comes from renewable portfolio standards (RPS) at the state level, which specify how much electricity must come from renewable sources. More ambitious renewable mandates stimulate greater battery adoption because rising shares of intermittent renewables widen the price spreads that batteries can exploit.

Electricity demand growth is another powerful force shaping the future of storage. Our simulations show that a 25 percent increase in peak-hour demand—holding other factors constant—could more than triple storage investment over the next decade. This finding underscores how storage may enable the expansion of energy-intensive digital infrastructure, such as data centers and artificial intelligence facilities.

Federal policy will also remain pivotal. Our simulations, calibrated to California’s market, suggest that the federal incentives alone—introduced by the 2022 Inflation Reduction Act and extended by the 2025 One Big Beautiful Bill Act—could, by 2024, have supported about the same level of early deployment as mandated under California state policy. Absent both the state requirement and federal support, most large-scale investments would likely have been postponed until much later in the decade.

Taken together, these results show how multiple forces interact to shape the path of storage investment. Renewable energy mandates increase the need for flexibility, demand growth from AI and data centers expands opportunities for profitable battery operation, and direct subsidies lower entry costs. The intersection of these trends will determine whether storage continues to expand rapidly or stalls in the coming years.

Main article

The 2025 One Big Beautiful Bill Act reshaped U.S. clean-energy incentives—extending the 30 percent tax credit for battery storage through 2033 while phasing out subsidies for solar and wind. This shift places storage at the center of the energy transition, just as electricity demand from data centers and AI is poised to surge. Using California as a case study, our research shows how federal subsidies, state policies, and electricity market dynamics interact to determine who gains, who loses, and how the next wave of storage investment will depend on future electricity demand and the durability of policy support.

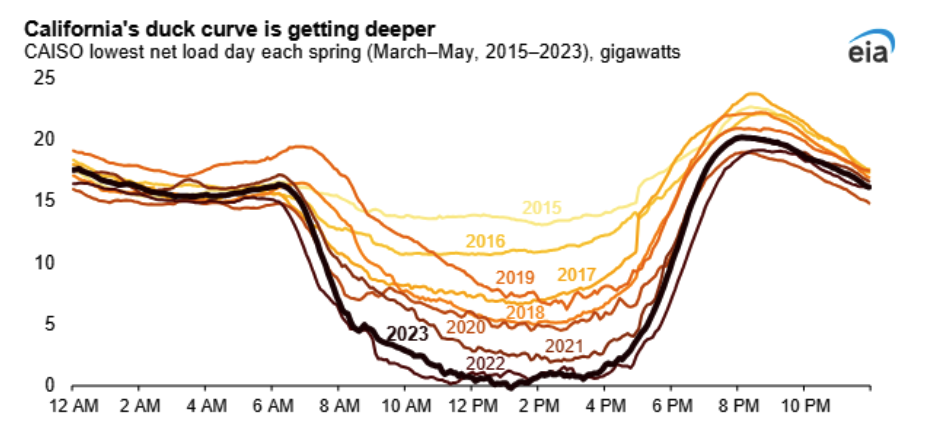

Renewable electricity generation has grown dramatically over the past decade in the U.S. and worldwide. By displacing fossil fuel generation, renewables reduce greenhouse gas emissions. However, most recent growth comes from intermittent sources like solar photovoltaics (PV), which cannot produce electricity after sunset or during cloudy periods. Without storage, integrating these sources requires backup generation that can ramp up quickly to meet the demand that exceeds the supply of solar and wind (i.e., net load) when renewable output falls—a phenomenon that has been colloquially referred to as the “Duck Curve” (see Figure 1). This challenge is likely to intensify as data centers and AI facilities come online, adding new electricity demand that will further test the grid’s ability to balance supply and demand across the day.

Figure 1

Notes: Net load is defined as total electricity demand minus electricity generated from renewable sources, primarily wind and solar. Image Source: EIA (2023).

This intermittency reduces the benefits of renewables because it intensifies the need for quickly adjustable and dispatchable types of generation, which are typically expensive and emission-intensive fossil fuel plants. Increasingly, renewable energy production is curtailed—grid operators must shut down solar plants even when the sun is shining—because production exceeds electricity demand. Indeed, Figure 1 shows this at 1 PM in 2023.

A small amount of battery storage would be profitable even without subsidies, but large-scale investment remains dependent on continued policy support.

Battery storage offers a promising solution: it can store excess energy when renewable output peaks and release it when production drops, ultimately lowering the overall costs of meeting electricity load. At the same time, battery costs have fallen sharply—lithium-ion cell prices dropped 85% from 2013 to 2024, with projections of further declines over the next decade (BloombergNEF, 2024). Despite these declines, capital costs remain a major barrier to utility-scale storage. As of 2024, utility-scale battery storage accounted for only about 2% of the U.S. generating capacity (EIA, 2024).

So, what role is battery storage likely to play in the future? How is this role shaped by the increase in reewable and intermittent generation sources? Are the current market incentives strong enough to support the entry of battery operators? What are the key forces that are likely to support or hinder the growth of battery storage? What are the likely effects of storage subsidies introduced in the 2022 Inflation Reduction Act and extended by the 2025 One Big Beautiful Bill Act?

To tackle these questions, we build a framework to understand both how batteries operate in the electricity market and how potential battery operators decide whether to add capacity to the grid. Our framework has two components that analyze these two parts. First, an operations model captures how battery operators make charge and discharge decisions. Every five minutes, each battery operator—acting as a price arbitrageur—decides whether to charge (buy electricity) or discharge (sell electricity), with the goal of maximizing expected future profits. This is inherently a dynamic and stochastic problem: each operator must weigh current prices against uncertain future price paths when deciding whether to hold its charge level, store energy, or release energy.

Second, an adoption model captures how potential investors decide when to enter the market. Each year, each potential operator makes an optimal stopping decision—choosing whether to install storage capacity now or wait—based on current capital costs, renewable energy mandates, the existing stock of battery capacity in the market, and expectations about future cost declines and battery stock.

Batteries smooth out extreme price swings—but in doing so, they erode the very profits that attract new investment.

We apply our framework to California, a state at the forefront of renewable energy production. We use data from the California Independent System Operator (CAISO) from 2016 to 2019, including day-ahead and real-time electricity prices, total load, generation by resource type, natural gas prices, and hydroelectric availability. These data, together with assessments on the costs of battery technology and engineering details such as the average battery duration and round-trip efficiency (which we obtain from the National Renewable Energy Laboratory), allow us to estimate batteries’ optimal operation decisions at every 5-minute interval over the four years of our data. During this period, California experienced dramatic growth in renewable generation—especially solar—which we leverage to identify the interaction between renewable generation and battery profitability.

To credibly answer our research questions, our framework needs to capture how electricity markets would behave if far more battery storage were operating than we observe. This matters because, as batteries become more common, they naturally smooth out extreme price swings—which, somewhat paradoxically, reduces the profits batteries can earn from buying low and selling high. We develop a method to predict how prices adjust when large-scale batteries operate in the market. This involves solving for a new equilibrium in which individual battery operators all continue to optimize while market prices respond to their presence. A key technological feature that we model is that traditional power plants face ramping costs: it is often cheaper for them to keep running than to shut down and restart, and these factors materially shape prices in a world with many more batteries. Our model also incorporates practical limits of lithium-ion technology, including energy losses when charging and discharging and the fact that frequent, deep cycling causes batteries to degrade over time.

The Promise and Limits of Large-Scale Battery Storage

Our first main finding is that a small amount of battery storage would be profitable even without subsidies, but large-scale investment remains dependent on continued policy support because of the paradoxical effect noted above.

Beyond profitability, storage also reshapes who gains and who loses in the electricity market.

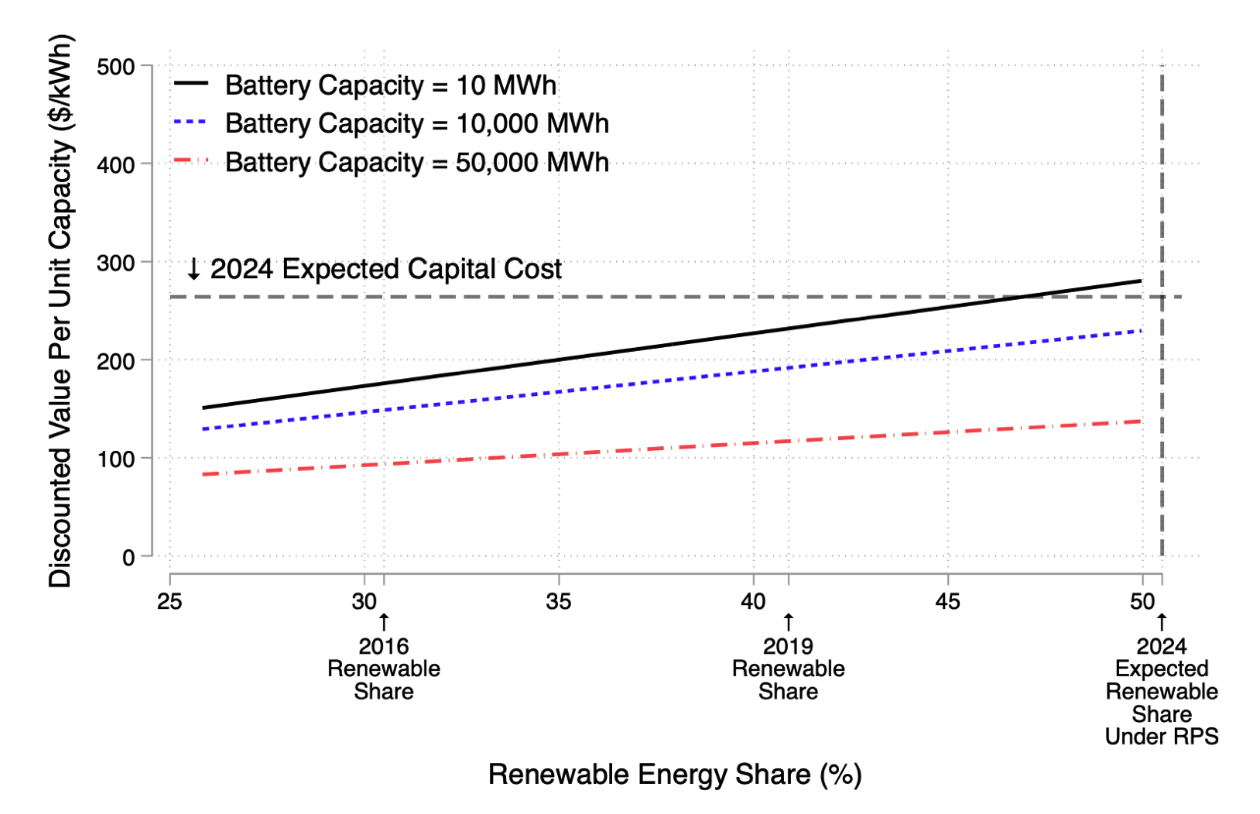

Figure 2 shows how the expected lifetime value of storage changes as renewable generation expands. When renewables supply about half of total electricity—roughly California’s level in 2024—a small fleet of batteries (10 MWh) can just break even, covering its capital cost of $264/kWh. But as total storage capacity grows, profits fall sharply because batteries compete with one another to arbitrage the same price fluctuations.

Figure 2

Notes: Each sloped line represents the best linear fit between weekly simulated values and renewable share for the respective capacity level. The gray horizontal line marks the projected 2024 capital cost of battery storage, while the vertical line indicates the expected renewable share under California’s RPS and authors’ calculations.

These diminishing returns are quantitatively large. At a 50 percent renewable share, average value per kilowatt-hour falls from about $280 for a 10 MWh fleet to $230 for 10,000 MWh and just $140 for 50,000 MWh. For this reason, modest investments can pay for themselves, but large-scale deployment is unlikely without subsidies or mandates.

There is a significant complementarity between battery adoption and renewable penetration.

Beyond profitability, storage also reshapes who gains and who loses in the electricity market. We find that 1,000 MWh of storage reduces annual revenues for dispatchable generators by about $126 million. Even solar and wind producers see a $14 million decline, as batteries depress prices during late-afternoon hours when solar output is still relatively high.

This pattern reflects the times of day when batteries buy and sell electricity. Operators tend to buy power in the middle of the day—when solar output is high, prices are low, and supply is relatively elastic—and to sell during the evening ramp hours, when solar generation drops and supply becomes tight. As a result, the price impacts follow a clear pattern: large declines in the evening, modest declines in the late afternoon, and slight increases around midday.

Policy, Demand Growth, and the Future of Storage

Our study also directly models how battery adoption may evolve under different policy and market environments. Investors adopt batteries when expected revenues from buying low and selling high outweigh installation costs and the risk that these profits will decline as more competitors enter. These incentives depend not just on technology costs, but also on the policy environment and the trajectory of electricity demand.

Demand growth from data centers and AI could more than triple storage investment over the next decade.

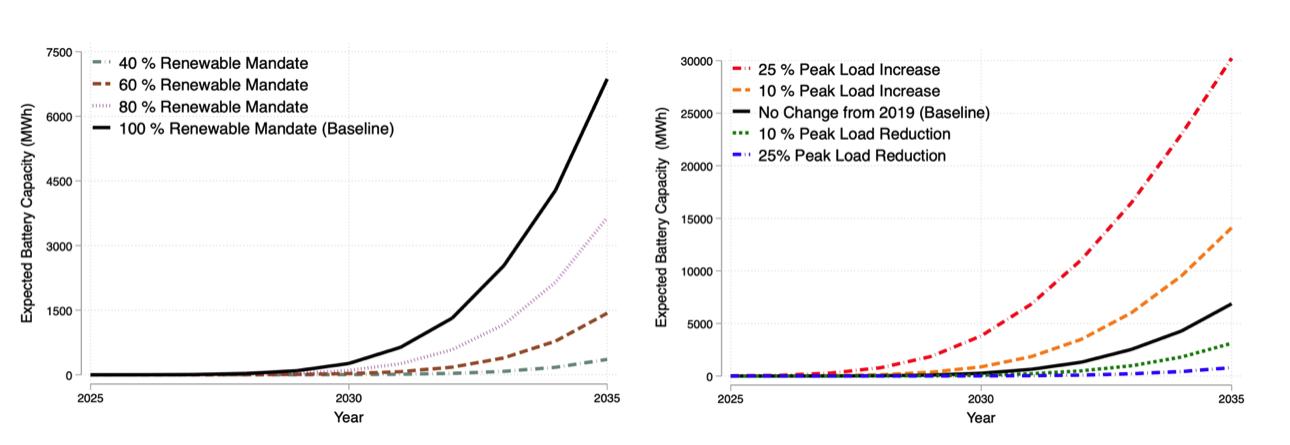

Specifically, we find that a major determinant of future adoption comes from renewable portfolio standards (RPS) at the state level, which specify how much electricity must come from renewable sources. These policies vary widely across the country: California has committed to reaching 100 percent clean electricity by 2045, while many states have weaker or no renewable targets. In our model, there is a significant complementarity between battery adoption and renewable penetration: more ambitious renewable mandates stimulate greater battery adoption because rising shares of intermittent renewables widen the price spreads that batteries can exploit. Figure 3’s first panel shows that while little storage is built under moderate renewable mandates, adoption rises sharply under stringent RPS policies.

Figure 3

Notes: Model projections of future battery storage capacity under alternative policy and market conditions. Panel A shows storage adoption rising with more ambitious state renewable portfolio standards, while Panel B illustrates that a 25 percent increase in peak-hour electricity demand could more than triple storage investment over the next decade.

We also find that electricity demand growth is another powerful force shaping the future of storage. The rapid buildout of data centers and artificial intelligence facilities could add significant new load to the grid. To the extent these data centers operate in the evening when solar output declines, this will boost the value of storage, as batteries can sell power during those peak hours. Our simulations show that a 25 percent increase in peak-hour demand—holding other factors constant—could more than triple storage investment over the next decade. This finding underscores how storage will not only help integrate renewables but may also enable the expansion of energy-intensive digital infrastructure.

Policy remains central to shaping the next phase of storage growth.

Federal policy will also remain pivotal. The 2022 Inflation Reduction Act first introduced subsidies for stand-alone storage, and the 2025 One Big Beautiful Bill Act extended those credits through 2033 even as incentives for solar and wind were phased out. This shift marks a new phase of U.S. energy policy—one focused on balancing generation and load rather than simply expanding renewable capacity. Our simulations, calibrated to California’s market, suggest that the 30 percent federal tax credit alone could have supported roughly 5,000 MWh of storage by 2024—even without the state’s mandate to procure this amount of storage (Assembly Bill 2514, 2010). In other words, the federal incentive on its own would have achieved about the same level of early deployment observed under California state policy. Absent both the state requirement and federal support, most large-scale investments would likely have been postponed until much later in the decade—underscoring how policy remains central to shaping the next phase of storage growth.

Taken together, these results show how multiple forces interact to shape the path of storage investment. Renewable energy mandates increase the need for flexibility, demand growth from AI and data centers expands opportunities for profitable battery operation, and direct subsidies lower entry costs. The intersection of these trends will determine whether storage continues to expand rapidly or stalls in the coming years.

This article summarizes ‘Soaking Up the Sun: Battery Investment, Renewable Energy, and Market Equilibrium’ by R. Andrew Butters, Jackson Dorsey, and Gautam Gowrisankaran, published in Econometrica in May 2025.

R. Andrew Butters is an associate professor and Blanche “Peg” Philpott Faculty Fellow at the Kelley School of Business, Indiana University. Jackson Dorsey is an assistant professor at the University of Texas at Austin Economics Department. Gautam Gowrisankaran is a professor of economics at the Columbia University Economics Department, and a research associate of the CEPR and NBER.

References:

- Butters, R. A., Dorsey, J., & Gowrisankaran, G. (2025). Soaking Up the Sun: Battery Investment, Renewable Energy, and Market Equilibrium. Econometrica, 93(3), 891-927. https://doi.org/10.3982/ECTA20411

- BloombergNEF (2024). Lithium-ion battery pack prices see largest drop since 2017, falling to $115 per kilowatt-hour. https://about.bnef.com/insights/commodities/lithium-ion-battery-pack-prices-see-largest-drop-since-2017-falling-to-115-per-kilowatt-hour-bloombergnef/.

- California Assembly Bill 2514, 2009-2010 Reg. Sess., Cal., 2010.

- U.S. Energy Information Administration (2023). As solar capacity grows, duck curves are getting deeper in California. Today in Energy, March 6, 2023. https://www.eia.gov/todayinenergy/detail.php?id=56880

- U.S. Energy Information Administration (2024). Battery storage makes up 2% of U.S. utility-scale generating capacity in 2024. Today in Energy. March 12, 2025. https://www.eia.gov/todayinenergy/detail.php?id=64705